Reporting on the EU Taxonomy

It aims to channel financing flows into investments that support sustainable development in the future. In this context, a new classification system for economic activities – the EU taxonomy – is to help investors assess whether investments contribute to political targets and obligations such as the Paris Agreement on climate change at the same time as meeting specified environmental and social standards. To this end, the EU has defined six categories, or objectives:

1. Climate change mitigation

2. Climate change adaptation

3. Sustainable use of water

4. Transition to a circular economy

5. Pollution prevention and control

6. Protection and restoration of biodiversity and ecosystems

The relevance of an economic activity for one of these environmental objectives depends on how the activity influences the respective environmental objective.

In order to assess an economic activity, a two-step analysis must be performed with regard to eligibility and alignment. To determine alignment, each activity must be assessed as to whether it makes a substantial contribution to any given objective of the EU taxonomy while doing no significant harm (DNSH) to any of the other objectives.

Moreover, minimum safeguards for compliance with human rights including labor and consumer rights and in the fields of bribery and corruption prevention, taxation and fair competition must be guaranteed for each activity.

Companies that fall within the scope of the EU taxonomy must disclose the defined sales, capital expenditure (CapEx) and operating expenditure (OpEx) ratios for their share of taxonomy-eligible or taxonomy-aligned economic activities. These ratios must be itemized according to the respective taxonomy-eligible or taxonomy-aligned economic activity. The disclosures must specify the envi-ronmental objective to which this activity contributes and whether it is a transitional or enabling economic activity.

Taxonomy-eligible activities at LANXESS

With regard to the environmental objectives “climate change mitigation” and “climate change adaptation,” the Taxonomy Regulation covers activities of selected economic sectors that are currently responsible for a total amount of around 93 % of European greenhouse gas (GHG) emissions. All of these activities are described as “taxonomy-eligible.” With regard to the “climate change mitigation” objective, the chemical industry is a “transformative industry” because, among other things, basic chemicals and plastics that are produced in very large quantities are labeled as transitional activities. This means that the activities make a relevant contribution to the EU’s GHG emissions and thus have relevant reduction potential. LANXESS – as a specialty chemicals company – is not focused on such products. Under the EU Taxonomy Regulation, all other activities that do not materially contribute to GHG emissions in the EU and accordingly are not defined in the Climate Delegated Act are currently labeled as “taxonomy-noneligible”. Criteria for the demonstration of “enabling activities” – i.e. activities that in turn enable third parties to make their own material positive contribution to climate change mitigation – have not yet been defined for the chemical industry.

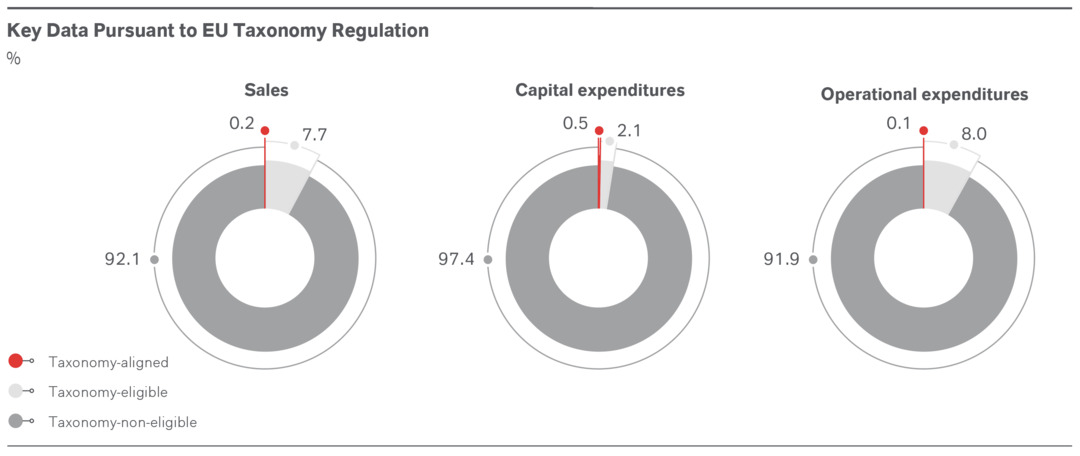

Reportable ratios for the fiscal year 2022

Sales

LANXESS generated 8 % of its external sales with products allocable to taxonomy-eligible activities. The remaining 92 % of sales relate to products that are not included in the taxonomy’s activity categories. Compared to the previous year, the share has decreased significantly as the taxonomy-eligible sales from the High Performance Materials (HPM) business are no longer reported as continuing operations.

Capital expenditures and operational expenditures

We report the proportion of expenditures and expenses incurred in connection with the operation and expansion of our plants in order to manufacture taxonomy-eligible products as taxonomy-eligible capital expenditures and operational expenditures.

Capital expenditures

The share of taxonomy-eligible capital expenditures was 3%. Therefore, the share of taxonomy non-eligible activities in our capital expenditures is 97 %. Due to our extensive M&A activities, we also report an additional ratio that we adjust for the influence of business acquisitions. In this analysis perspective, the taxonomy-eligible share increases to 5 % and now reflects the capital expenditures attributable in 2022 to plants that manufacture the taxonomy-eligible products.

The share of taxonomy-eligible capital expenditures was 3%. Therefore, the share of taxonomy non-eligible activities in our capital expenditures is 97%. Due to our extensive M&A activities, we also report an additional ratio that we adjust for the influence of business acquisitions. In this analysis perspective, the taxonomy-eligible share increases to 5 % and now reflects the capital expenditures attributable in 2022 to plants that manufacture the taxonomy-eligible products.

Operational expenditures

In accordance with the Taxonomy Regulation, the ratio’s denominator must cover direct non-capitalized costs that relate to research and development, building renovation measures, short-term leases, maintenance and repair. Any other direct expenditures relating to the day-to-day servicing of assets of property, plant and equipment by the company itself or third parties must also be included.

The share of operational expenditures for taxonomy-eligible products amounted to 8 % of the total operating expenditures. Therefore, the share of taxonomy non-eligible operating expenditures is 92 %. The share of taxonomy-compliant operating expenses amounts to 0.1 % of our operating expenses.

LANXESS

LANXESS